Hartman Group: Pleasure & distinction bigger drivers than health for premium products

The premium food opportunity: When are US consumers most likely to trade up?

In the latest Hartbeat Exec report, Hartman Group CEO Laurie Demeritt and James Richardson, Ph.D. SVP, Knowledge & Innovation, at Hartman Strategy note that “while premium M&A activity heats up, the reality is that consumers are concentrating their trade up dollars in food and beverage far more in some categories than in others.”

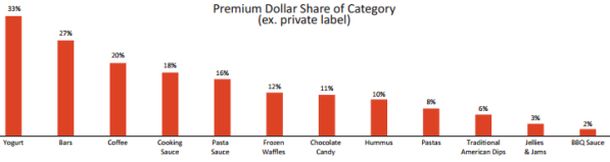

For example, premium brands typically account for around 12% of the dollar share in most food & beverage categories (excluding private label), but the variance is huge (from just 2% for BBQ sauce to 33% for yogurt).

- Yogurt 33%

- Bars 27%

- Coffee 20%

- Cooking sauce 18%

- Pasta sauce 16%

- Frozen waffles 12%

- Chocolate candy 11%

- Hummus 10%

- Pastas 8%

- Traditional American Dips 6%

- Jellies & Jams 3%

- BBQ sauce 2%

Source: Hartman Strategy, using Nielsen total US XAOC data 52 weeks ending July 5, 2014. EXCLUDES private label

Indeed, in some categories where premium penetration is ultra-low, they add, “Retailers may not really understand the need among their shoppers for anything else beyond a simple natural organic private label offering.

“Categories with a low premium share are often declining volumetrically, suggesting innovating into premium when a category is losing its relevance in food culture overall is a mixed bet.”

Similarly, you may be wasting your time trying to build a premium brand in a “culturally cold” or “off-trend” category, they claim: “It is hard to get excited about reinventing refrigerated ranch dip.”

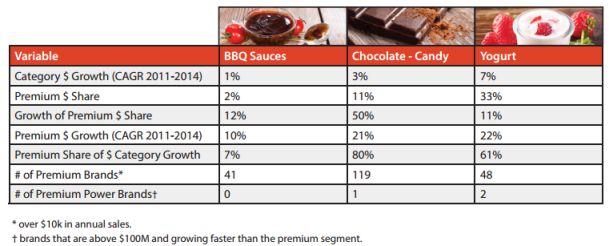

However, there are pockets of opportunity, say the authors, notably hummus, “the powerhouse premium segment with the most promise for acceleration of market share."

Why do consumers buy premium food and beverage products?

Consumers’ motivations for buying premium products vary by category. But indulgence, pleasure, distinction and artisanal qualities are probably stronger selling points than health claims in most premium categories, including chocolate, despite the interest in cocoa flavanols, suggest the authors.

“Health & wellness is functioning more as a rationalization…” (Consider red wine, they point out. Although many of us are aware of its heart health benefits, there is little evidence that we’re really drinking the stuff for all that resveratrol.)

“It is critical for premium offerings to sell pleasure and distinction first and foremost.”

'Breakout premium brands' singled out by Hartman Group include:

- Noosa (indulgent yogurt): "Noosa is challenging the ascetic dieting/weight management legacy of the yogurt category. The result is a full-fat, super-indulgent yogurt with 280 calories per serving, growing exponentially in a category where low fat and nonfat still dominate... Consumers have moved beyond fear of fat and are seeking out healthy fats in moderation. Whole-milk dairy products are joining butter, avocados, olive oil and other sources of ‘good fats’ in contemporary food culture."

- Eat Well Embrace Life ('other bean hummus'): "Eat Well Embrace Life is hoping to stretch the nutrient-dense credentials of hummus into a broader format play."

- Nature's Bakery (Fig Bars): "The fig bar is not new, but one devoid of conventional R&D additives is.. This features 100% real figs and a very thick, dense layer of whole grains that set it far apart from its more iconic inspiration."

- Theo (gourmet chocolate): "While its conventional channel performance is driven on more mainstream flavors, the presence of artisanal product runs reinforces the credibility of the brand’s claims to premium quality."

Read the full report: Market Dynamics of the New Premium